It is hard to believe we are halfway through 2026, and are seeing some distinct trends throughout our sample markets in the Los Angeles area. Below are YTD stats on pricing, days on the market, months of inventory and list-to-sale ratios with commentary on each.

If you have any questions or if I can be of assistance to you, please do not hesitate to reach out.

Jonathan

818.469.5309 | jonathan@sheishoperealty.com

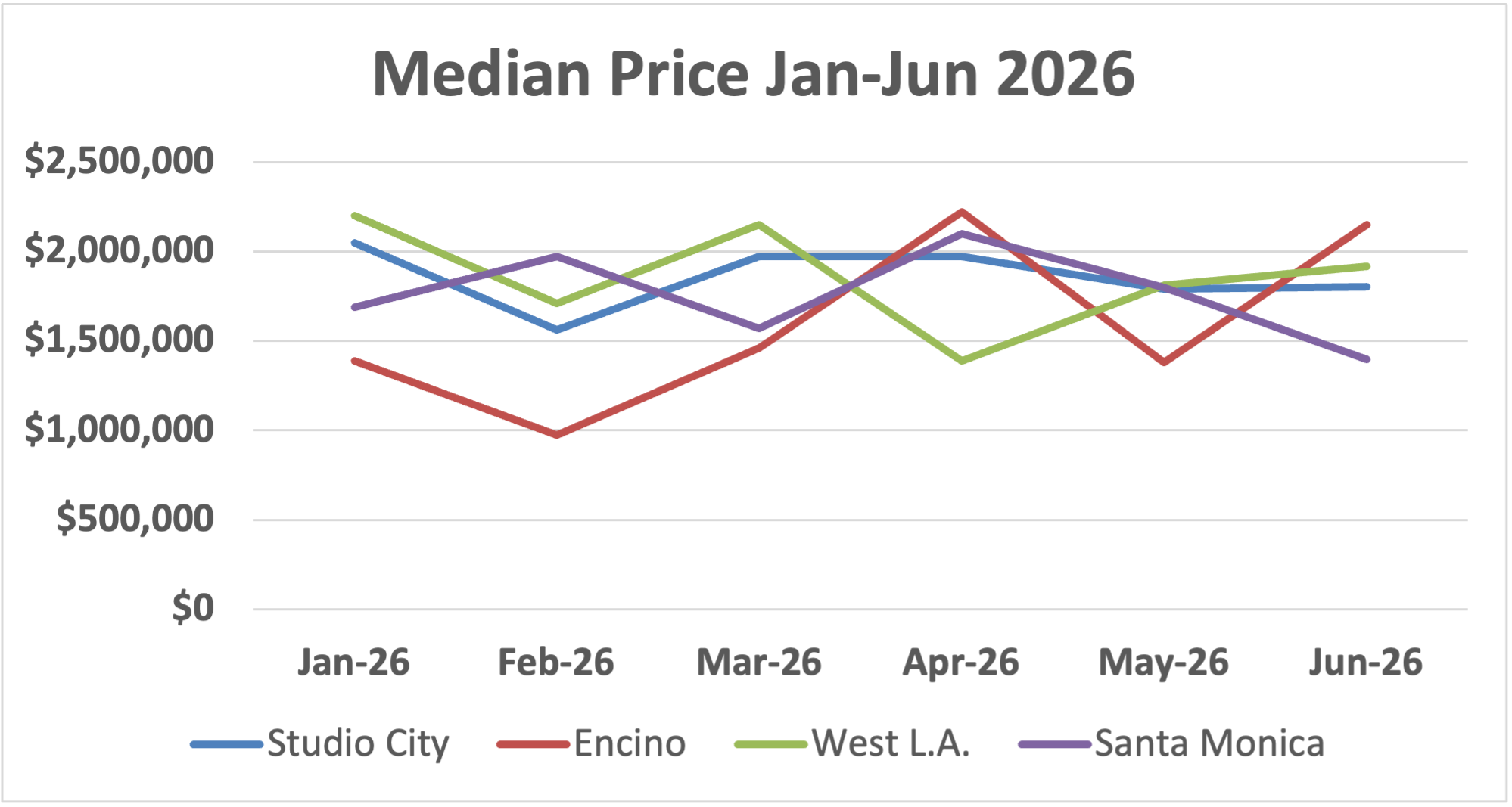

Pricing is seeing some volatility in the first half of 2026

Pricing across our sample markets has been volatile in the first half of 2026 - three of four markets ended June below their January median, with Studio City down approximately 12%, West LA down 13%, and Santa Monica down 17% on a January-to-June basis. Encino moved sharply in the opposite direction, though its month-to-month swings, from $975K in February to $2.2M in April, reflect the nature of relatively higher priced inventory, where a handful of transactions can move the median significantly in either direction. For context, LA County overall was essentially flat YTD at $950K, with broader market stability that these higher home-value markets segment have not mirrored.

Key takeaways:

- Accurate pricing at the initial list price is more essential than ever; the data does not support testing the market with an aggressive number.

- Month-to-month volatility means pricing decisions should be anchored in a range of comparable sales over time vs. a single month's median.

- The adage 'The risk of overpricing is greater than the risk of underpricing' is more true than ever. Homes priced above the market will generally take longer to sell.

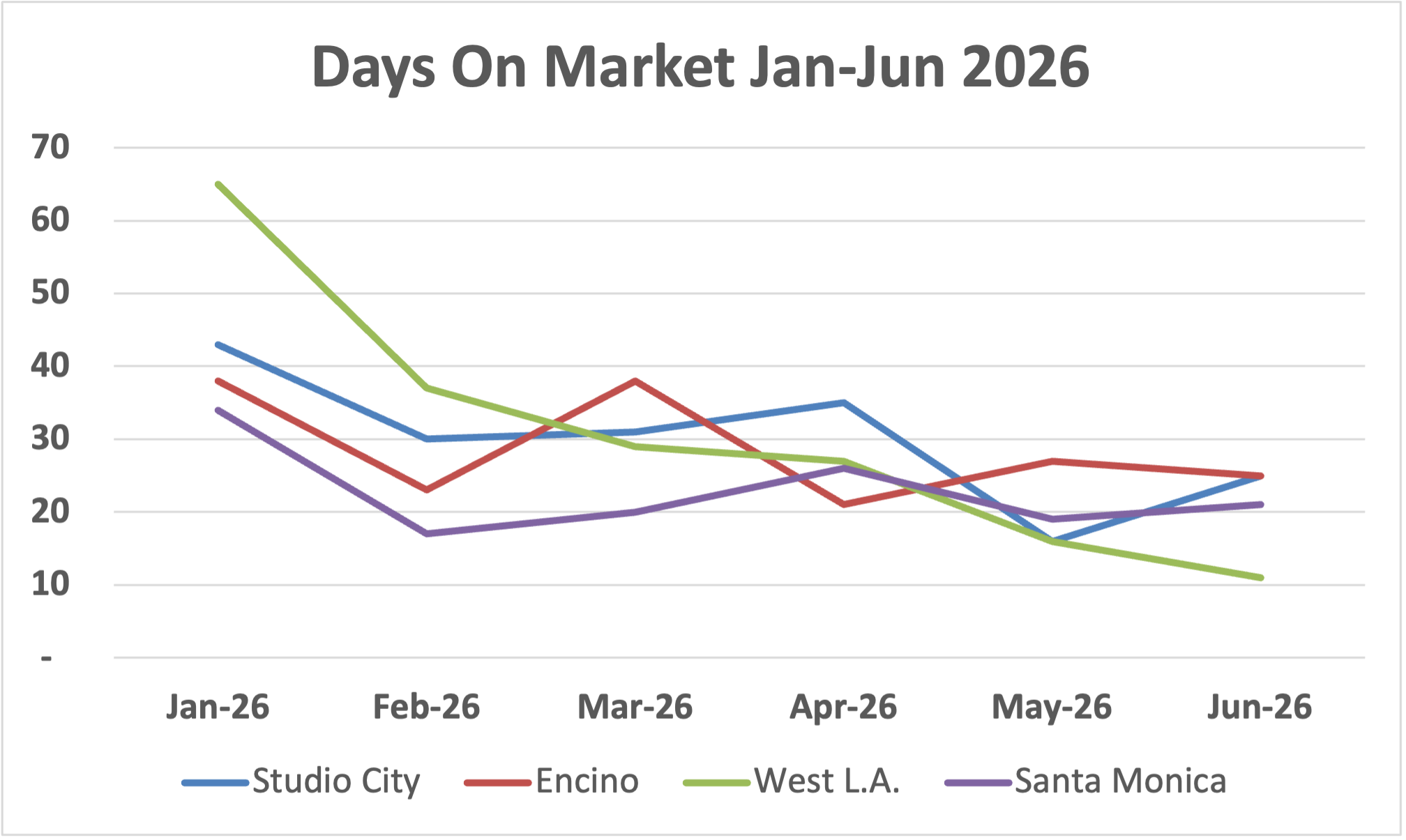

Days on the market are trending lower

The most consistent positive signal in the H1 data is that homes are selling faster in June than they were in January across all four markets. West LA compressed from 65 days in January to 11 days in June in a dramatic shift. Studio City moved from 43 days to 25, Encino from 38 to 25, and Santa Monica from 34 to 21. June did see a slight moderation in some markets relative to May's lows, moderating the trend, but the directional improvement means buyer activity picked up meaningfully through the spring, and well-positioned listings are moving.

Key takeaways:

- DOM compression is happening, but requires the right pricing and preparation. Homes that arrive on market ready to show are driving these numbers.

- A listing that sits past the market's median DOM loses negotiating leverage quickly; the first two weeks remain the most valuable window.

- Pricing and presentation work together to generate foot traffic.

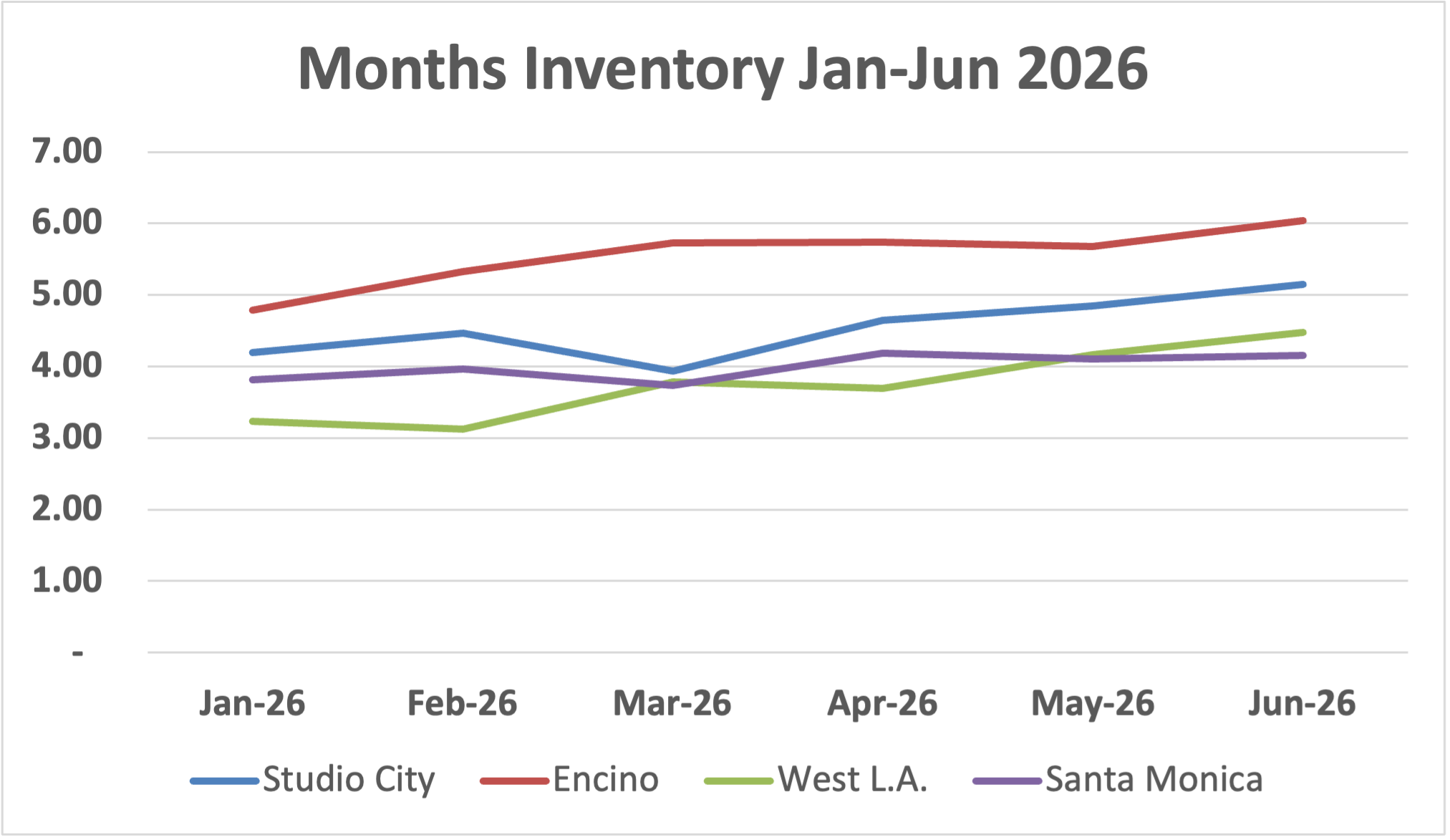

Conversely, inventory has been increasing YTD

Inventory rose in every single market across H1, without exception. Studio City moved from 4.19 months in January to 5.15 in June; West LA from 3.23 to 4.48; Santa Monica from 3.81 to 4.15; and Encino from 4.79 to 6.04. This rising inventory trend is something to keep watch on; inventory accumulating on the sidelines largely reflects homes priced ahead of where buyers are willing to go.

Key takeaways:

- Rising inventory means more competition for seller attention; differentiation matters more than it did a year ago.

- Encino at 6.04 months is at equilibrium; sellers in that market should expect a more balanced negotiating dynamic than in prior years.

- Watch this metric alongside DOM through Q3: if inventory continues rising while DOM holds steady or increases, this could create more opportunities for buyers.

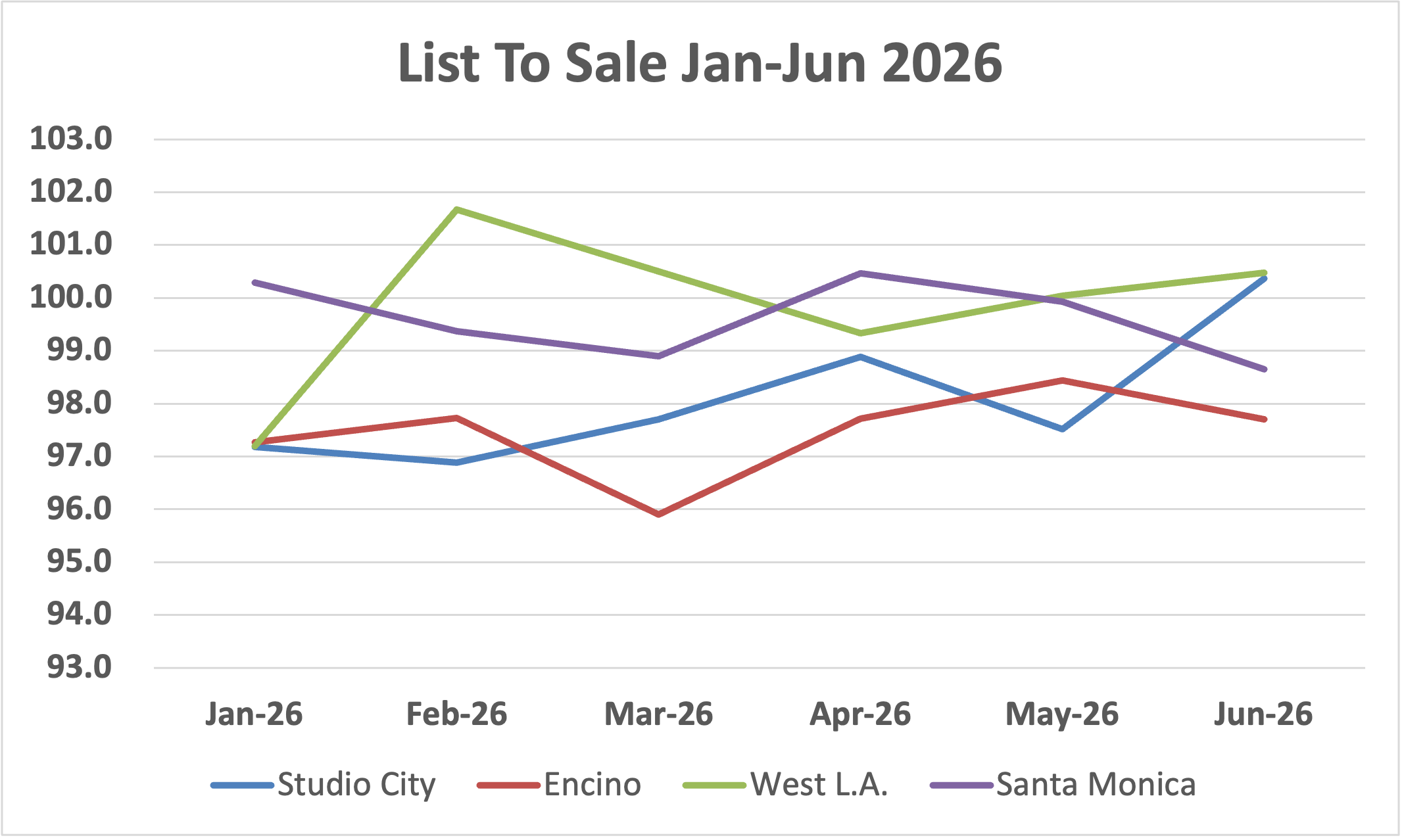

List-to-sale ratio has remained relatively steady

List-to-sale ratios across all four markets held in a narrow 96-101% band for the entire first half of 2026, the most stable metric in the dataset. June closed with Studio City at 100.37% and West LA at 100.47%, meaning the median sale exceeded asking price. Santa Monica (98.65%) and Encino (97.70%) closed June just under asking, within a tight negotiating range. This is a precise market that rewards disciplined pricing from the start.

Key takeaways:

- A list-to-sale ratio near or above 100% reflects accurate initial pricing, and a recognition of where the market is sitting.

- Buyers in all four markets should expect limited room for significant discounting on well-priced inventory, but could find opportunities with homes listed above the current market.